SBA Form 2483

Audio By Carbonatix

Advertising Can't Do It Alone

The challenges facing local news organizations are very real. That's why reader support matters more than ever. If you believe independent journalism matters, make a contribution today and help us reach our summer fundraising goal of $12,500 by August 9.

Congress grunted out a steaming pile of legislation known as the Coronavirus Aid, Relief, and Economic Security Act, or CARES Act, on March 27.

First off, can we please stop with these horribly tortured acronyms for legislation names? They all remind me of the USA-PATRIOT Act, which reminds me to be angry at a whole other administration of fools and crooks. Bet you forgot that one was an acronym.

CARES is the kind of garbage you get when Democrats who don’t care about you meet Republicans who actually want you to die.

Congress’ message to us is, “have zero health care, no rent relief, no mortgage relief, no comprehensive pandemic response, and best of luck in the upcoming respirator wars. Here’s $1,200 not to notice that we bailed out the corporations again.”

But there is one small part of the act I kind of like. The Paycheck Protection Program is aimed at helping small businesses keep people employed. Also, it’s merely alliterative, not an acronym.

My mind jumped instantly to the restaurant operators we’ve been highlighting in the Observer who are trying to keep staff employed making take-out and delivery food. If PPP can help them, maybe I can get my weight under control not trying to keep them all open by myself.

If your business qualifies, you can get a forgivable loan equal to 2.5 times your average monthly payroll cost up to $10 million to be used on paying employees.

Two and a half months of payroll doesn’t hold a candle to what other developed countries are doing to support workers, but it’s a lot better than the absolutely-fucking-nothing small business got in the financial crisis, and it might mean the difference between survival and failure for some businesses.

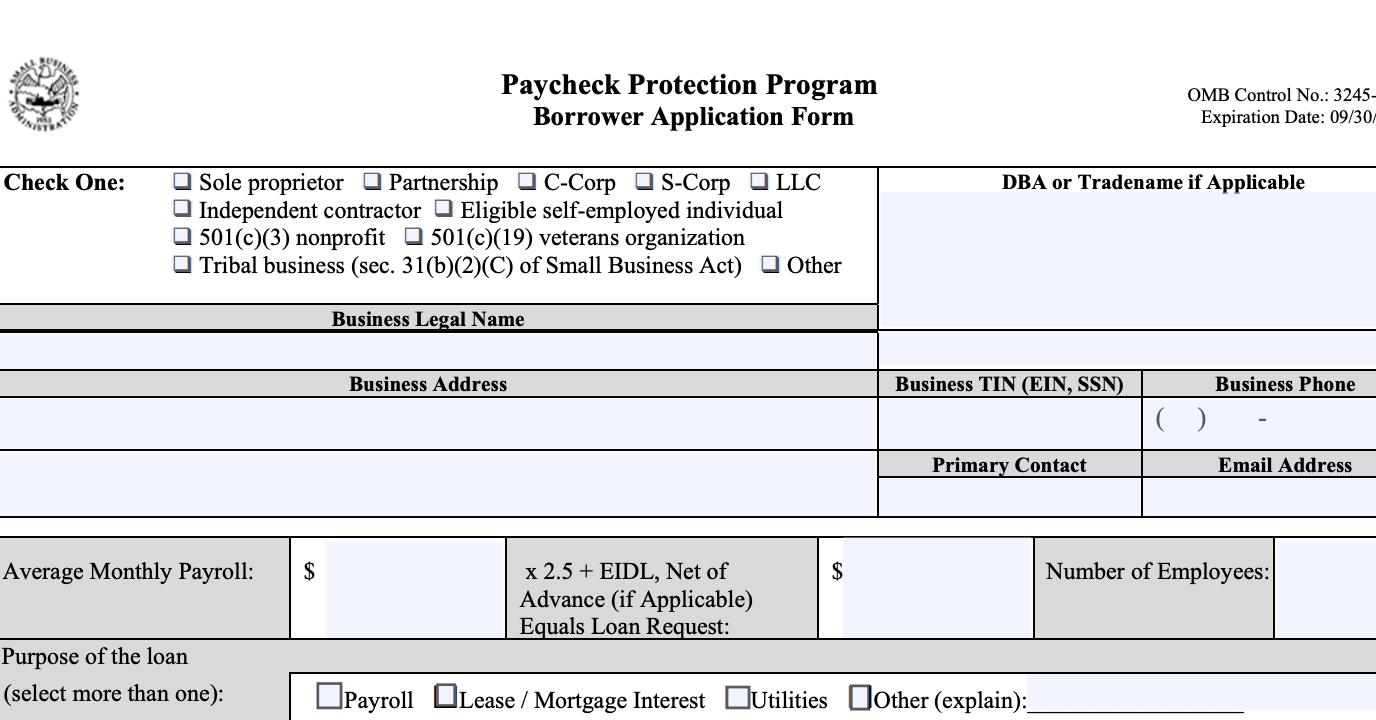

Here’s supposedly the final version of the application.

Two caveats: 1) I got it from treasury secretary Steve Mnuchin’s Twitter feed and 2) Treasury and the SBA are fighting over the details of PPP. I know; you’re shocked that the administration can’t roll this out smoothly.

Here’s more detail I cribbed from Melissa Kingston. Hey, if you were quarantined with a badass employment lawyer, would you look this up yourself?

Eligibility

– Business must have been operating on Feb. 15, 2020

– Business (broadly defined to include things like 501(c)(3)s) must have fewer than 500 employees or otherwise meet SBA’s size standard

– If you are in the accommodation and food services sector, 500 employee rule applies per location

– If you are operating as a franchise or receive funds from an approved Small Business Investment Company, the normal affiliation rules do not apply

– Individuals who operate sole proprietorship, are self-employed, or work as independent contractors

How It Works:

– Lenders participating in the program will determine whether you qualify and for how much, and they will process the loan.

– Currently approved SBA lenders can issue loans

– SBA is working on rules to add additional lenders

– If you already have an SBA loan, you can apply for another under this act, but proceeds cannot be for same uses

What Will Lenders Look For:

– Lenders will look for documentation that shows that you meet the eligibility requirements

– Lenders will ask for a certification from you that:

– The uncertainty of current economic conditions makes the loan necessary

– You will use loan proceeds to pay workers and make necessary mortgage/lease and utility payments

– You do not have any other similar loan applications pending with other lenders

– For independent contractors, sole proprietorships and the self-employed, lenders will need documents like payroll tax filings, Forms 1099, and other similar income and expense verification documents

– Lenders will not require:

– Proof that borrower has sought and been denied credit elsewhere

– A personal guaranty

– Collateral for the loan

How Much Can You Borrow:

– Loans can be up to 2.5 times borrower’s average monthly payroll costs, not to exceed $10 million

– “Average payroll costs” is defined differently, depending on whether the business was operational in 2019 or just 2020 and whether employees are seasonal employees

> There is a formula for calculating “payroll costs”

– Included: payments of any compensation to employees that is:

– Salary, wage, commission or similar pay

– Payment of cash tips or the equivalent

– Paid benefits, like vacation, sick leave, etc.

– Payments made for severance or separation

– Employer’s share of insurance payments (e.g., health insurance)

– Employer’s share of retirement plan contributions

– State or local tax assessed on the compensation of the employee

– Not Included:

– Compensation to any individual employee in excess of $100,000 (prorated Feb. 15 – June 30, 2020)

– Payroll taxes and income taxes

– Compensation to any employee whose principal place of residence is outside the US

– Qualified sick leave or family leave payments made under the Families First Coronavirus Response Act

– Payroll Costs = sum of included payroll costs – sum of excluded payroll costs

Loan Forgiveness

> Borrower is eligible for loan forgiveness equal to the amount borrower spent on the following items during the 8-week period beginning on the date of the origination of the loan:

– Payroll costs (above)

– Interest on mortgage obligations incurred in the ordinary course of business

– Rent on leased equipment

– Payments on utilities

– For borrowers of tipped employees, additional wages paid to them

> Reductions to Loan Forgiveness

– Forgiveness can be reduced if you reduce the number of employees or reduce wages more than 25%

– Reductions in employees or wages that occurred between Feb. 15, 2020 and 30 days after the CARES Act was passed (March 27, 2020) will not be grounds to reduce loan forgiveness if, by June 30, 2020, the number of employees and/or wages are restored

> Amounts Not Forgiven – for loans that are not forgiven, permitted terms are:

– Maximum term of loan is 10 years

– Maximum interest rate is 4%

– No loan fees

– Prepayment fees are limited by SBA

– Payments are deferred for six months (interest still accruing) after forgiveness period